Loading...

Join our Facebook Group: Join: Expats in Poland

Loading...

Value-added tax (VAT) in Poland is a consumption tax that businesses charge on goods and services. The standard VAT rate in Poland is 23%, with reduced rates of 8% and 5% for certain items. VAT represents a significant portion of Poland's revenue, accounting for about 40% of its total tax earnings.

Value-added tax (VAT) is a consumption tax levied on the value added to goods and services at each stage of production or distribution. Unlike a simple sales tax, VAT is collected incrementally, based on the surplus value added to a product by a business at each stage of production. This system ensures that tax is paid at every step of the supply chain, making it one of the most efficient forms of indirect taxation.

In Poland, VAT is a crucial component of the tax system, contributing significantly to government revenue. Understanding VAT is essential for businesses operating in Poland, as it affects pricing, cash flow, and compliance obligations. Whether you're a small entrepreneur or running a large corporation, proper VAT management is vital for legal compliance and financial planning.

Understanding VAT obligations and compliance in Poland.

Photo: Tax documentation and calculation

When you purchase goods or services in Poland, you pay VAT in addition to the net price. For businesses, VAT operates on a system of input and output tax, creating a chain of tax collection throughout the supply process. This mechanism ensures that the final consumer bears the full VAT burden while businesses act as intermediaries in the collection process.

The VAT system includes Output VAT (charged on your sales to customers), Input VAT (paid on your business purchases), and your VAT liability (Output VAT minus Input VAT). If positive, you pay the difference to tax authorities; if negative, you receive a refund. This system prevents double taxation and ensures businesses only pay VAT on the value they add to products or services.

In Poland, businesses with annual turnover exceeding 200,000 PLN must register for VAT and charge it on all sales. However, smaller businesses can opt to be exempt from VAT obligations under certain conditions, similar to small business regulations in other EU countries. This exemption can provide administrative relief and potentially competitive pricing advantages for qualifying businesses.

Important to note: VAT-exempt businesses cannot reclaim input VAT they've paid on their purchases. This trade-off between administrative simplicity and VAT recovery should be carefully considered when deciding whether to register voluntarily for VAT or remain exempt under the small business threshold.

Poland's EU membership means special VAT rules apply for cross-border transactions. Intra-EU B2B sales typically qualify for 0% VAT, provided proper documentation and valid EU VAT numbers are obtained. This facilitates trade within the European Union while maintaining tax compliance across different member states.

For businesses selling to consumers in other EU countries, distance selling thresholds apply. Once you exceed 10,000 EUR in sales to consumers in another EU country, you must register for VAT in that country or use the One Stop Shop (OSS) scheme for simplified reporting.

Digital services have special rules where the customer's location determines the applicable VAT rate, regardless of where your business is established. Understanding these international VAT obligations is crucial for businesses operating across EU borders or serving international customers from Poland.

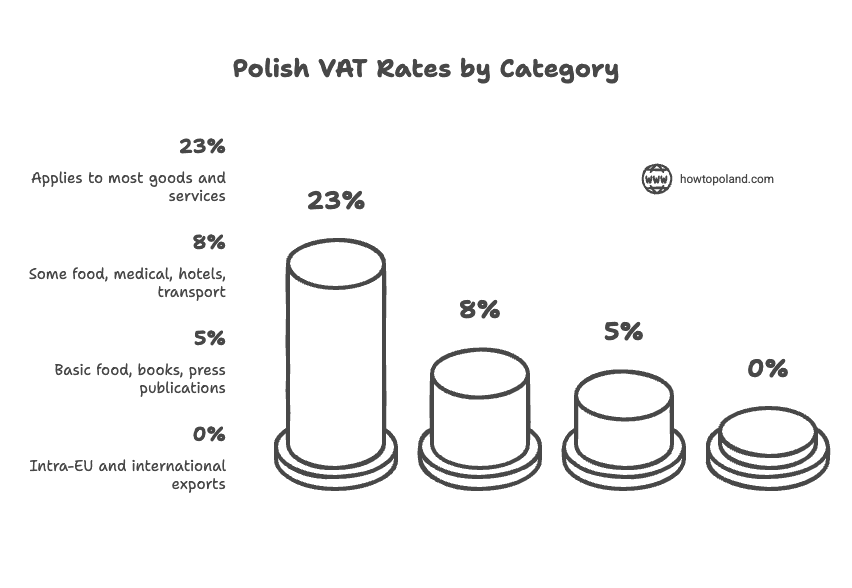

Poland applies four different VAT rates depending on the type of goods or services provided. The standard rate is 23% for most goods and services, including electronics, clothing, professional services, and hospitality. This is one of the higher VAT rates in the European Union, reflecting Poland's fiscal policy approach.

Reduced rates of 8% and 5% apply to essential goods and services. The 8% rate covers selected foods, pharmaceuticals, medical devices, books, newspapers, takeaway food, hotel accommodation, and public transport. The super-reduced 5% rate applies to basic foods like bread, milk, meat, fruits, and vegetables.

A 0% rate applies to exports outside the EU, international transport, and certain medical services. Understanding which rate applies to your business is crucial for proper pricing and VAT compliance. When in doubt, consult the Polish tax authorities (KAS) or a qualified tax advisor, as VAT rates can change based on government policy.

Infographic: Polish VAT Rate Structure

| Rate | Category | Specific Examples |

|---|---|---|

| 23% | Standard rate | Electronics (phones, laptops, TVs), clothing and footwear, furniture, cars and car parts, cosmetics and perfumes, alcohol, tobacco, professional services (legal, consulting, IT, marketing), construction materials, household appliances, jewelry, toys |

| 8% | Reduced rate | Hotel accommodation, restaurant and takeaway food, pharmaceuticals (OTC and prescription), medical devices, printed books and e-books (educational), newspapers and magazines, public transport (bus, tram, metro), construction/renovation of residential buildings (up to 300m2), certain agricultural supplies, cleaning services for residential buildings |

| 5% | Super-reduced rate | Basic food: bread and bakery products, milk and dairy, fresh meat and poultry, fish, fruits and vegetables, eggs, cereals, rice, pasta, baby food, juices (100% fruit/vegetable), printed books and certain periodicals, sheet music |

| 0% | Zero rate | Exports of goods outside the EU (with customs documentation), intra-EU supply of goods (to VAT-registered buyers with valid EU VAT ID), international transport of passengers and goods, certain medical equipment for hospitals, humanitarian aid supplies |

Note: Some products may fall under different rates depending on specific circumstances. For example, food sold in a restaurant is taxed at 8%, but the same food bought in a supermarket may be 5%. Always verify the correct rate for your specific product or service with the Polish classification system (PKWiU).

Polish taxes can be confusing for foreigners. Get matched with an accountant who speaks English and knows the rules for expats.

Tax filing support

PIT, CIT, VAT returns handled correctly - avoid penalties and overpayment

Fluent in English

No language barrier - discuss your finances clearly and get advice you understand

Expat tax expertise

Double taxation treaties, foreign income, ZUS obligations - they know the specifics

Free matching

No cost to you - we connect you with the right accountant for your situation

VAT registration in Poland depends on your business turnover and strategic choices. Understanding when registration is mandatory versus voluntary, and the implications of each option, is crucial for proper business planning and tax compliance.

Annual turnover exceeds 200,000 PLN

Must register before starting business activity or within 14 days of exceeding the threshold.

Once your business crosses the 200,000 PLN annual threshold, VAT registration becomes mandatory. This applies whether you're a sole trader, partnership, or corporation. The registration process is straightforward but must be completed promptly to avoid penalties.

Annual turnover below 200,000 PLN

Can choose to register voluntarily to reclaim input VAT on business expenses.

Voluntary registration can be beneficial if you have significant business expenses with VAT. However, once registered, you're committed to charging VAT on all sales and filing regular returns, even if your turnover remains below the threshold.

Since April 1, 2026, every VAT-registered business in Poland must issue B2B invoices through KSeF (Krajowy System e-Faktur), the National e-Invoicing System operated by the Ministry of Finance. Large taxpayers with sales above 200 million PLN have been required to use it since February 1, 2026, and the smallest micro-entrepreneurs join on January 1, 2027.

KSeF replaces paper and PDF invoices for B2B transactions and is closely tied to your VAT registration. Read our complete KSeF guide for the rollout schedule, authentication methods, penalties, and how to get started.

Polish VAT identification numbers follow the standardized EU format: PL1234567890. This number is essential for all VAT-related transactions and must appear on invoices for business-to-business sales.

JPK-V7 (Jednolity Plik Kontrolny) is Poland's mandatory electronic reporting format that every VAT-registered taxpayer must submit. Introduced in October 2020, it replaced the separate VAT-7 declaration and JPK_VAT file, combining them into a single report that the tax office uses for automated verification of your transactions.

The JPK-V7 file consists of two main parts:

Declaration Part (Deklaracja)

Records Part (Ewidencja)

Most accounting software in Poland (e.g., wFirma, Fakturownia, Comarch ERP) can generate and submit JPK-V7 files automatically. If you use an accountant, they handle JPK-V7 filing as part of their standard bookkeeping service. For more about your tax obligations, see our guides on income tax rates and ZUS social security contributions.

The reverse charge mechanism shifts the obligation to account for VAT from the seller to the buyer. Instead of the seller charging VAT on the invoice, the buyer self-assesses VAT and reports both output and input VAT in their own JPK-V7 filing. This is common in cross-border B2B transactions and prevents the need for foreign companies to register for VAT in Poland.

When a foreign company provides services to a Polish VAT-registered business, the Polish buyer must account for VAT using reverse charge.

Common examples:

The Polish buyer must:

A Polish IT company hires a German graphic designer for 1,000 EUR. The German designer issues an invoice without VAT (reverse charge applies). The Polish company must self-assess 23% VAT = 230 EUR, reporting it as both output and input VAT in their JPK-V7. If the Polish company has full VAT deduction rights, the net cost is zero - but the reporting obligation is mandatory. Failure to report reverse charge properly can result in penalties during a tax audit.

Poland's EU membership means specific VAT rules govern cross-border trade with other member states. These rules differ for goods versus services, and for B2B versus B2C transactions. Getting them right is essential to avoid double taxation or unexpected VAT liabilities.

If you sell goods or digital services to consumers (not businesses) in other EU countries and exceed the 10,000 EUR annual threshold, you must charge VAT at the buyer's country rate. Instead of registering for VAT in every EU country where your customers live, you can use the OSS system:

Selling Services to EU Businesses (B2B)

Selling Services to EU Consumers (B2C)

Foreign businesses that incurred Polish VAT on business expenses (e.g., hotel stays, conference fees, car rentals) but are not VAT-registered in Poland can reclaim that VAT through a refund procedure. The process differs depending on whether the company is based in the EU or outside it.

Directive 2008/9/EC procedure

13th Directive procedure

Typically Refundable

Typically NOT Refundable

Poland's standard 23% VAT rate is above the EU average. Here's how it compares to other member states. This is particularly relevant for businesses operating across borders or considering where to establish their EU base.

| Country | Standard Rate | Reduced Rate(s) |

|---|---|---|

| Poland | 23% | 8%, 5% |

| Hungary | 27% | 18%, 5% |

| Denmark | 25% | - |

| Sweden | 25% | 12%, 6% |

| Italy | 22% | 10%, 5%, 4% |

| Belgium | 21% | 12%, 6% |

| Netherlands | 21% | 9% |

| Czech Republic | 21% | 12% |

| Spain | 21% | 10%, 4% |

| France | 20% | 10%, 5.5%, 2.1% |

| Austria | 20% | 13%, 10% |

| Germany | 19% | 7% |

| Romania | 19% | 9%, 5% |

| Luxembourg | 17% | 14%, 8%, 3% |

Rates shown as of 2026. Hungary has the highest standard VAT rate in the EU at 27%, while Luxembourg has the lowest at 17%. Poland sits in the upper-middle range. For businesses selling to consumers across the EU, the destination country's rate applies (when using OSS). For B2B transactions, VAT is handled via reverse charge regardless of rate differences.

You must register for VAT if your annual turnover exceeds 200,000 PLN. Below this threshold, registration is voluntary but can be beneficial if you want to reclaim VAT on business expenses. New businesses should carefully consider their expected revenue and business model when deciding on VAT registration.

The standard VAT rate in Poland is 23%, which applies to most goods and services. However, there are reduced rates of 8% for certain items like books and pharmaceuticals, 5% for basic food products, and 0% for exports and some essential services. Always check which rate applies to your specific products or services.

Only if you're VAT-registered. Small businesses with turnover below 200,000 PLN that choose to remain VAT-exempt cannot reclaim input VAT on purchases. However, you can voluntarily register for VAT to reclaim input VAT, though this means you must charge VAT on all sales and file regular returns.

Most businesses file monthly VAT returns by the 25th of the following month. Small businesses with annual turnover below 1.2 million PLN can apply for quarterly filing. All returns must be submitted electronically through the tax office's online system or approved accounting software.

You must register for VAT within 14 days of exceeding 200,000 PLN in annual turnover and start charging VAT immediately. You'll need to issue corrective invoices for recent sales where VAT should have been charged. It's important to monitor your turnover throughout the year to avoid penalties.

For B2B services to VAT-registered businesses in other EU countries, you typically charge 0% VAT using the reverse charge mechanism. For B2C services, you may need to charge the customer's country VAT rate. Digital services to consumers always follow the destination principle. Always verify the customer's VAT status and applicable rules.

You'll need to complete the VAT-R form, provide your business registration documents, proof of address, and identification. EU citizens need their passport or ID card, while non-EU citizens may need additional residence permits. The process can usually be completed online or at your local tax office.

Yes, if your turnover falls below 200,000 PLN and you were voluntarily registered, you can apply to cancel your VAT registration. However, you must remain registered for at least 12 months after voluntary registration. If you were mandatorily registered, you can only cancel if your turnover stays below the threshold for a full year.

JPK-V7 (Jednolity Plik Kontrolny) is Poland's Standard Audit File for Tax that combines the old VAT-7 declaration with detailed transaction records. Every VAT-registered business must file it electronically by the 25th of the month following the reporting period. Monthly filers use JPK_V7M; quarterly filers use JPK_V7K. Late or incorrect filing can result in penalties up to 500 PLN per error.